Universal Social Charge - Calculations

Some important points relating to the calculation of the Universal Social Charge (USC):

- The Universal Social Charge is collected in the same manner as PAYE and on the same calculation basis

- There is no USC relief on pension contributions

- USC is payable on gross income, including Notional Pay, before employee pension contributions.

Employers are notified of the specific USC deduction method for each individual employee in the same manner as they are notified about an employee's PAYE deductions, i.e. on the Revenue Payroll Notification (RPN) on an employee by employee basis.

USC Exemption Marker

Where Revenue determine that the employee/pensioner’s total annual earnings (from all USC-able sources) will not exceed the USC exemption threshold currently, €13,000, the USC exemption will be stated on the RPN issued by Revenue. This USC exemption marker is an instruction to the employer/pension provider not to deduct USC from payments being made.

Where the employer holds an RPN which does not show exemption and the employee/pensioner advises them that USC exemption applies to them, the employee/pensioner should be instructed to contact their local Revenue office to arrange to have a revised RPN issued. While awaiting a revised RPN the employer should continue to use the RPN currently held.

Where the employer holds an RPN which does not show exemption and the employee/pensioner advises them that USC exemption applies to them, the employee/pensioner should be instructed to contact their local Revenue office to arrange to have a revised RPN issued. While awaiting a revised RPN the employer should continue to use the RPN currently held.

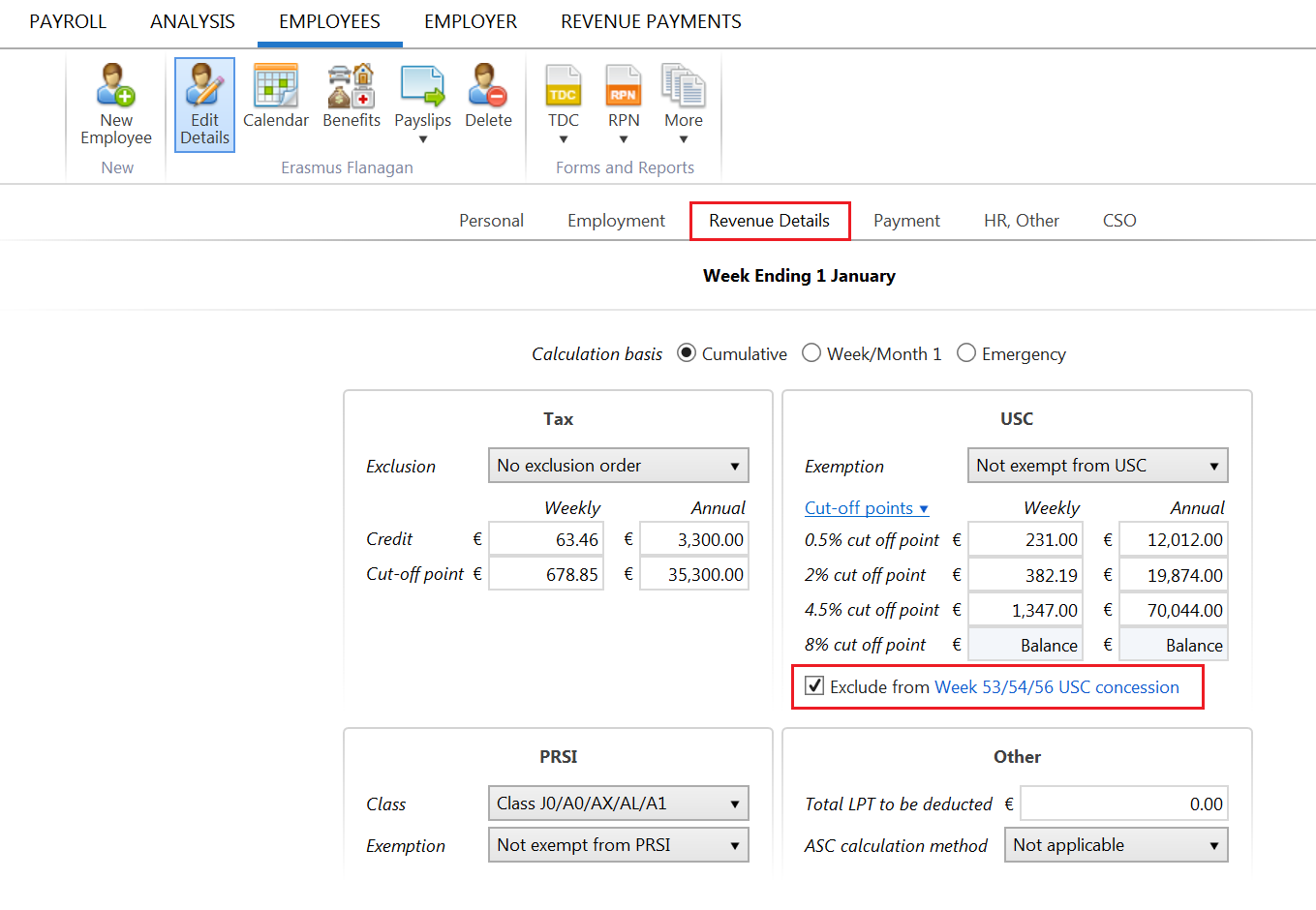

Calculating USC on Week 53

Where a week 53 occurs an additional period of USC threshold is allocated to the employee on a week 1 basis.

Please note: if an employee's normal pay day has changed during this tax year or the preceding tax year, the additional USC cut off points do not apply.

In this instance, you will need to instruct the software if the additional USC cut off points are not applicable to an employee.

To prevent the additional USC cut off points being allocated, go to:

Employees > Select the employee > Click their Revenue Details tab > Tick to exclude the employee from the week 53/54/56 USC concession > Save the change.

Need help? Support is available at 01 8352074 or brightpayirelandsupport@brightsg.com.

2025 BrightPay - System RequirementsBright ID2025 Budget - Employer Summary2025 BrightPay - AvailabilityIntroduction to BrightPayStarting the New Tax YearImporting from the Previous Tax YearInstalling BrightPayMoving from Thesaurus Payroll Manager to BrightPayMoving to BrightPay from another payroll softwareMoving BrightPay to a new PCBureau Enhancements - Additional FunctionalityEmployer SetupDigital CertificatesEmployee SetupRevenue Payroll Notifications (RPNs)Payroll CalendarProcessing PayrollImporting Pay Data from a CSV FilePayroll Deductions

PAYEPRSILocal Property Tax (LPT)USC

Payroll Submission Requests (PSRs)Distributing PayslipsPaying EmployeesSEPA format - Banks catered for in BrightPayMaking Corrections to PayrollRevenue PaymentsRevenue - Contact Telephone NumbersAnalysisPayroll JournalsProcessing StartersProcessing LeaversBenefit in KindIllness BenefitParenting BenefitsPensionsSwitching an Employee's Pay FrequencyBacking Up & Restoring Data FilesYear EndLeave Reporting & Employee CalendarAnnual LeaveLeave EntitlementsEmployment LawCSOGlossary of Terms (Pre 2019) - Foreign Language Help SheetsBrightPay ConnectGDPRBright Terms and Conditions and BrightPay End User Licence AgreementEnhanced Reporting Requirements (ERR)BrightExpensesTPM v BP - Employee recordsTPM v BP - Running the payrollBP v TPMUniversal Social Charge (USC) - General InformationUniversal Social Charge - CalculationsUSC Exempt Status v USC Exempt Income

Additional Superannuation Contribution (ASC)