IT IS IMPORTANT TO READ THE FOLLOWING NOTES CAREFULLY BEFORE PROCEEDING.

IMPORTANT NOTES ON BENEFIT IN KIND

PAYE, USC & PRSI must be operated by employers in respect of the taxable value of most benefits in kind and other non-cash benefits provided by them to their employees. The amount to be taken into account is referred to as "notional pay".

SMALL NON-CASH BENEFITS NOT EXCEEDING €250

Where an employer provides a small non-cash benefit (that is a benefit not exceeding €250) PAYE, USC & PRSI need not be applied to that benefit. No more than one such benefit given to an employee in a tax year will qualify for such treatment. Where a benefit exceeds €250 in value the full value of the benefit is subjected to PAYE, USC & PRSI.

Employer provided on-site Crèche/ Childcare facilities

Previously, where an employer provided day care facilities for employees on premises, this benefit carried a Benefit in Kind exemption. Budget 2011 abolished this exemption.

Employers now have to record the cost of this benefit, by relevant employee, within their payroll in order to deduct tax, USC and PRSI from the employee's pay.

Employers can use the Annual facility to enter the start date and value of this benefit.

Professional Subscriptions paid by Employer on behalf of an employee

Previously, where an employer paid professional subscriptions on behalf of an employee, this benefit carried a Benefit in Kind exemption. Budget 2011 abolished this exemption.

Employers now have to record any professional subscription payments made on behalf of an employee as a benefit.

Employers can use the Annual facility to enter the start date and value of this benefit.

EXEMPT ANNUAL BENEFITS

In the case of subscriptions paid on behalf of an employee, it is the expense incurred by the employer less any reimbursement by the employee that is taken into account for PAYE, USC & PRSI purposes.

Sports Facilities

Where sports facilities are made available on the employer’s premises for the use of employees generally, a taxable benefit does NOT arise. The facility must be available to ALL employees.

Employee required to live on premises

A taxable benefit will NOT arise where an employee (not director) is required by terms of his or her employment to live in accommodation provided by the employer in part of the employers business premises so that the employee can properly perform his or her duties, i.e. night care staff, governors, chaplains in prisons, caretakers etc.

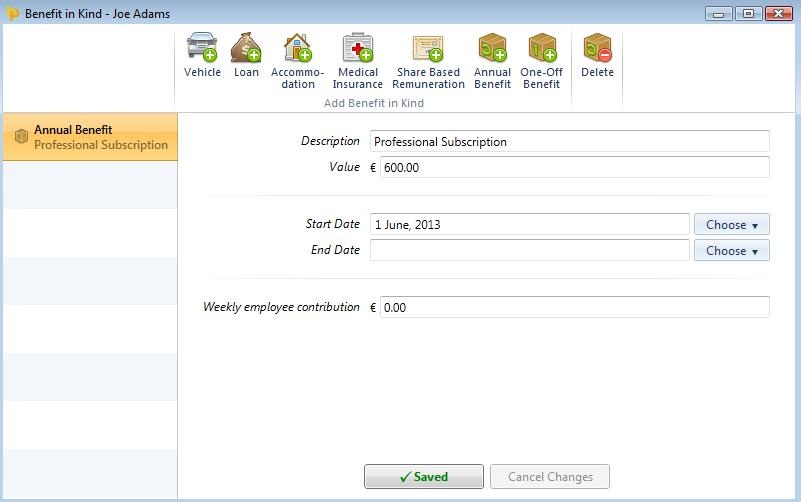

To access this utility go to Employees, select the employee in question from the listing and click Benefits on the menu toolbar, followed by Annual Benefit.

1) Description - enter a description of the annual benefit being provided.

2) Value – enter the value of the benefit being provided.

3) Start Date - enter the start date of the benefit provided.

4) End Date - enter the end date of the benefit provided if this ceases within the same tax year.

5) Employee contribution - enter any amount made good by the employee directly to the employer towards the cost of providing the benefit.

6) Click Save to save the Benefit In Kind entry.

The 'Notional Pay' will be added to the employee's gross income each pay period to ensure that the correct PAYE, Universal Social Charge and PRSI are charged.

Need help? Support is available at 01 8352074 or [email protected].

Copyright © 2025 Thesaurus Software Ltd T/A Bright Software Group.

Unit 35 Duleek Business Park, Duleek, County Meath, A92 N15E, Ireland

[email protected] 01 8352074