Operating EWSS in BrightPay

The Employment Wage Subsidy Scheme (EWSS) has replaced the Temporary Wage Subsidy Scheme (TWSS) from September 1st 2020.

Comprehensive Revenue guidance has been published with regard to the operation of the Employment Wage Subsidy Scheme.

It is recommended that you fully familiarise yourself with the Scheme Guidelines.

Employers must also determine that they meet the Scheme's qualifying criteria. If so, employers will then be required to register for the EWSS via ROS before they can avail of the Scheme.

Further information on the qualifying criteria can be found on the Revenue website .

In addition, Revenue have published guidelines on eligibility for the Employment Wage Subsidy Scheme from 1 July 2021 which can be accessed here

Important note

Employers must undertake a review of their eligibility for the scheme on the last day of every month (other than the final month of the scheme) to be satisfied whether they continue to meet the eligibility criteria and to take the necessary action of withdrawing from the scheme where they do not.

To assist employers in ensuring continued eligibility for the scheme, from 30 June 2021, all employers are required to complete and submit through ROS an online monthly EWSS Eligibility Review Form. Comprehensive guidance regarding this requirement can be found in Revenue's published guidelines which can be accessed here.

An overview of the Scheme is available here.

EWSS & BrightPay

Although the EWSS is a subsidy payable to employers only and will not impact employee payslips, the scheme must still be administered through the payroll.

The steps to complete within the software are provided below.

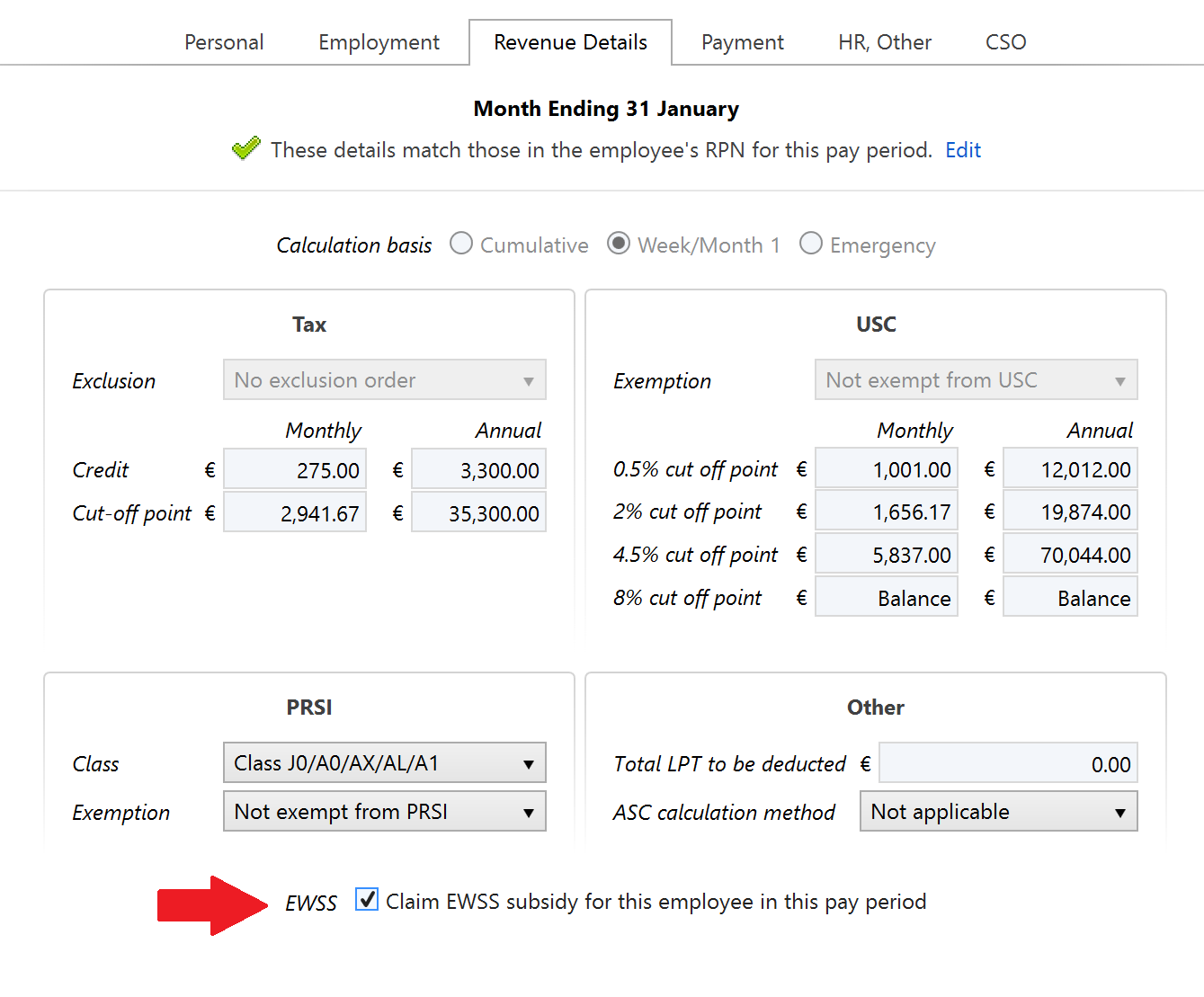

Step 1 - Indicate which employees are eligible for EWSS

a) If an employee is eligible to be claimed for under EWSS, you can instruct BrightPay that you wish to claim for them. This instruction will place an EWSS marker on the payroll submission (PSR) for that employee in order to notify Revenue that you wish to claim EWSS for them.

- Select Employees > choose the Employee > select their Revenue Details section

- Simply tick that you wish to 'claim EWSS subsidy for this employee in this pay period'

- Click 'Save Changes'.

b) Repeat the same steps above for each applicable employee.

Step 2 - Process your Payroll

After performing the above steps, you are now ready to process your payroll.

Under EWSS, employers are required to pay the employee as normal, calculating income tax, employee PRSI and USC in the normal manner.

On finalising each pay run, your associated payroll submission (PSR) will notify Revenue of the employees you wish to claim EWSS for. Submit this to Revenue in the normal manner.

On receipt of your payroll submission, Revenue will then determine the applicable subsidy amount payable.

Important Notes to the above:

- EWSS is a subsidy paid to the employer only and therefore there is no requirement to show EWSS on employee payslips.

- EWSS will also not show in an employee's myAccount.

- When processing your payroll, the software is programmed to take into account any lower and upper EWSS pay limits.

Where an employee's gross pay amount is outside of the limits and they have been marked as being an eligible employee for EWSS, the EWSS marker will not be included on the associated payroll submission for that employee.

(Gross pay includes notional pay and is before any deductions for pension, salary sacrifice etc.)

Where it is detected that the employee's gross pay is outside the limits, this will be brought to your attention on your employee's open payslip:

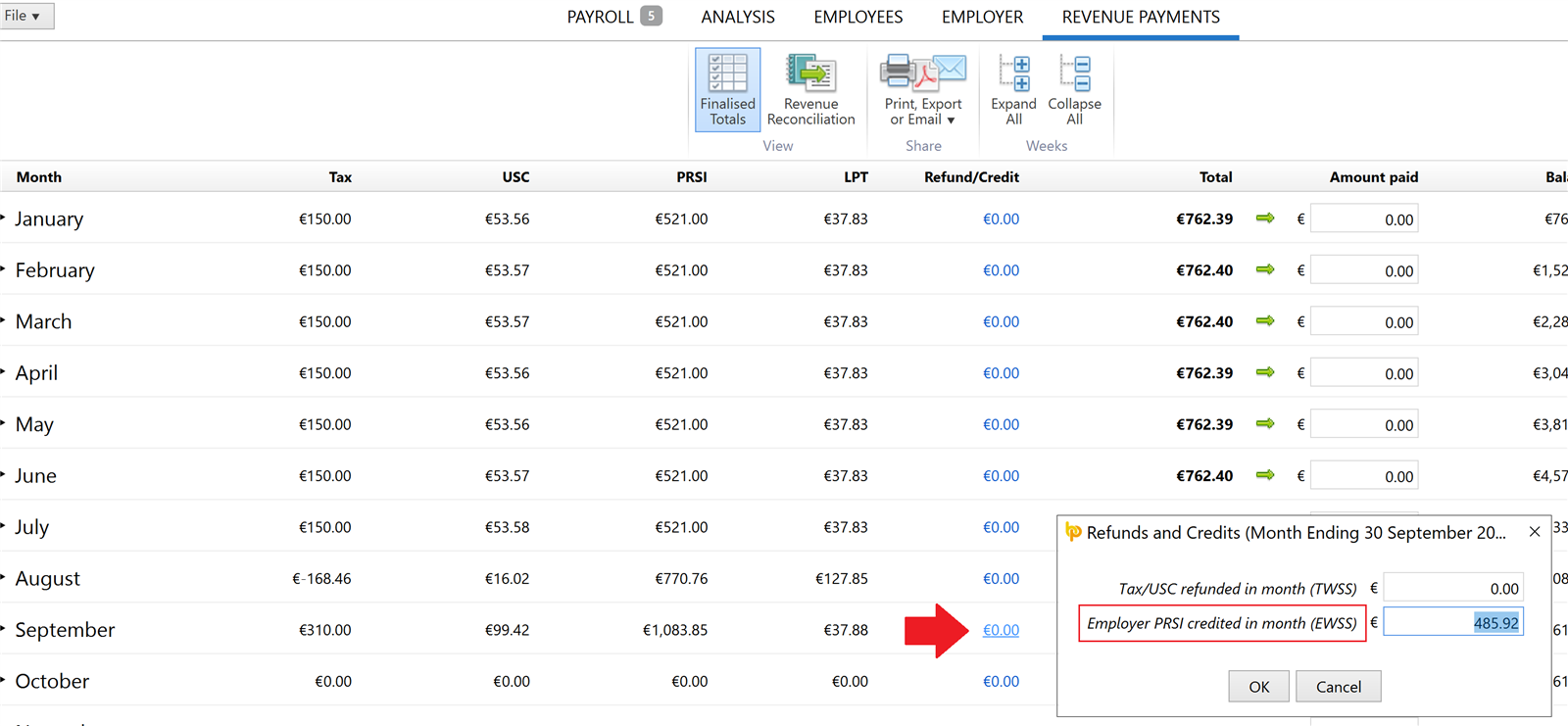

4. Up until the end of February 2022, a 0.5% rate of employer PRSI applies to employments that are eligible for the subsidy.

Employer PRSI however must be calculated as normal via payroll e.g. on PRSI class A1. Revenue will subsequently calculate a PRSI credit by calculating the difference between the employee's rate reported via the payroll submission and the 0.5%.

This credit will then show on the Statement of Account within ROS and reduce the employer’s liability to Revenue.

On confirmation of the PRSI Credit, users may wish to balance their Revenue Payments utility by entering the amount credited to them as follows:

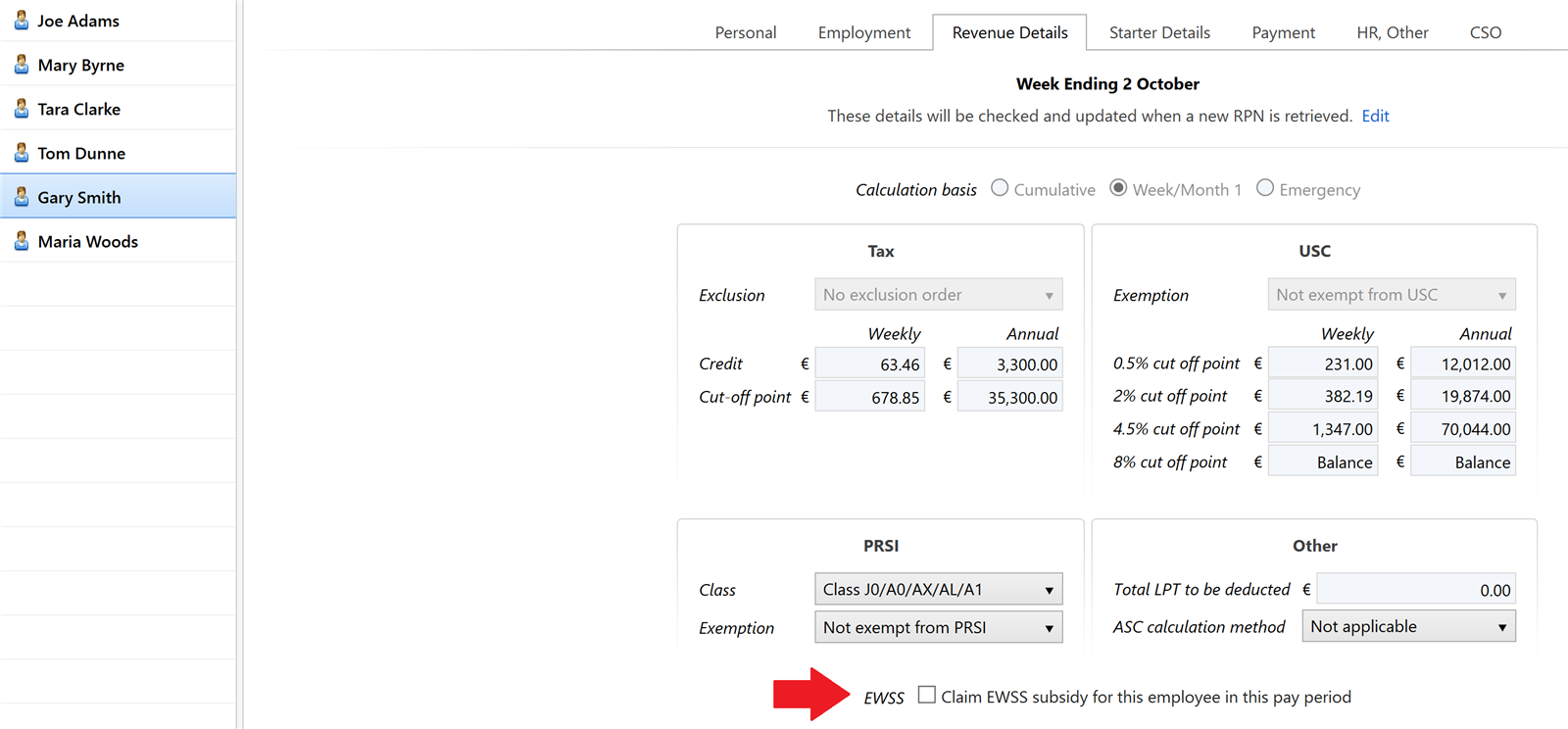

Step 3 - Monitor your EWSS Eligibility

Employers must review their eligibility status on the last day of every month to ensure they continue to meet the eligibility criteria.

Where you no longer qualify, you should de-register for EWSS with effect from the following day (1st of the month).

In this instance, you must also instruct BrightPay that you wish to stop claiming EWSS for your employees.

To do this, simply remove the EWSS marker from each applicable employee's record:

- go to Employees > choose the Employee > select their Revenue Details section

- Untick the option 'Claim EWSS subsidy for this employee in this pay period'

- Click Save Changes and repeat for each applicable employee

Alternatively, users may wish to use the Edit Settings option on the employee's payslip to access their Revenue Details section and untick the EWSS marker:

Please note:

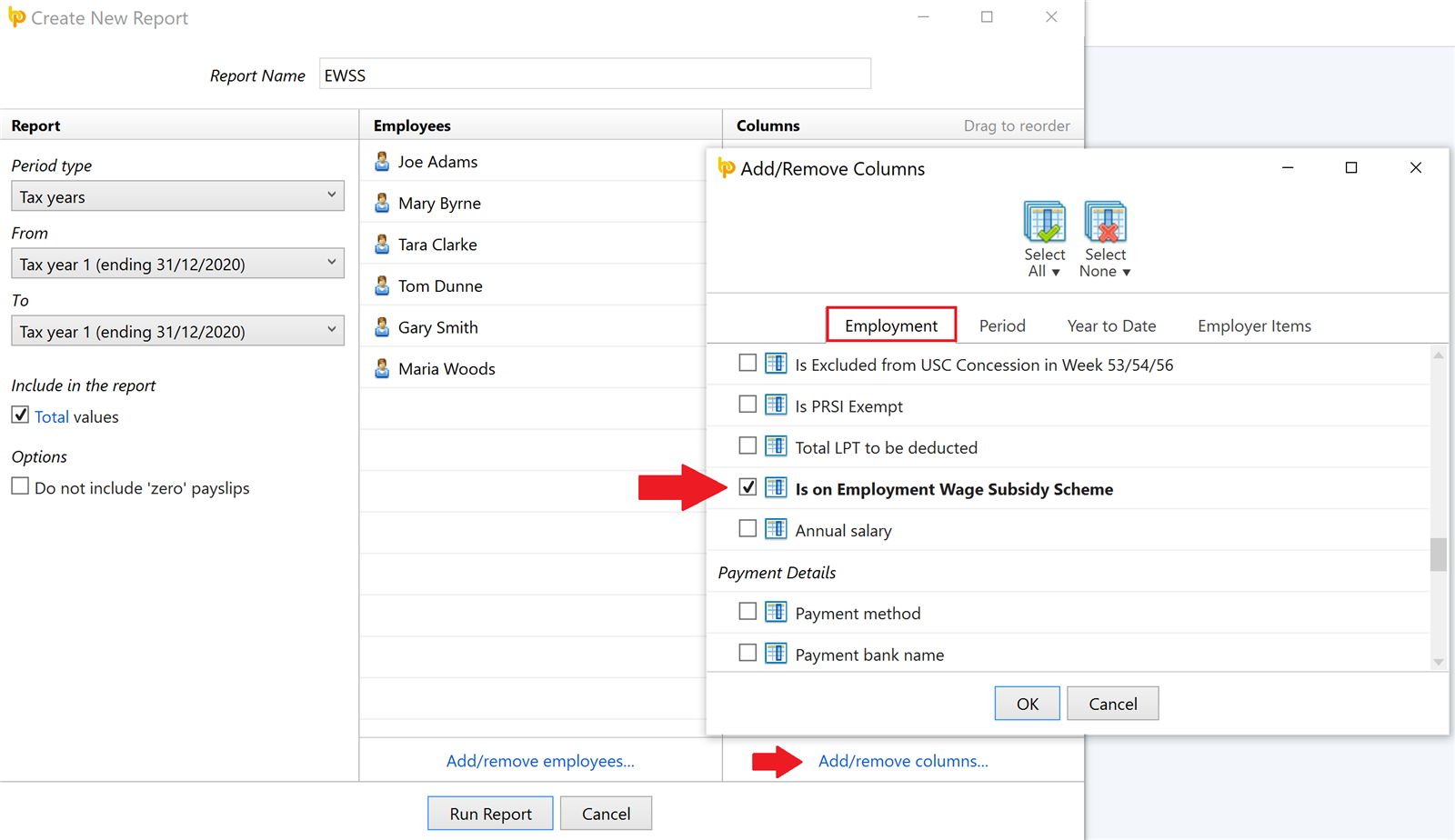

To assist users in ascertaining which employees the EWSS subsidy is currently being claimed for and who therefore require un-ticking, a report can be created and run within the Analysis function, as per the following example:

- Go to Analysis > New Report:

Need help? Support is available at 01 8352074 or brightpayirelandsupport@brightsg.com.